Closing Entries: Step by Step Guide

Interim periods are usually monthly, quarterly, or half-yearly. Income and expenses are closed to a temporary clearing account, usually Income Summary. Afterwards, withdrawal or dividend accounts are also closed to the capital account.

- The cyclical reporting of accounting periods can span monthly, quarterly, and annual time frames.

- Temporary account balances can be shifted directly to the retained earnings account or an intermediate account known as the income summary account.

- This is an optional stepin the accounting cycle that you will learn about in futurecourses.

- It’s vital in business to keep a detailed record of your accounts.

- The process of closing entries in accounting ensures the temporary accounts have a balance of zero at the end of the period.

Step 2: Transfer Expenses

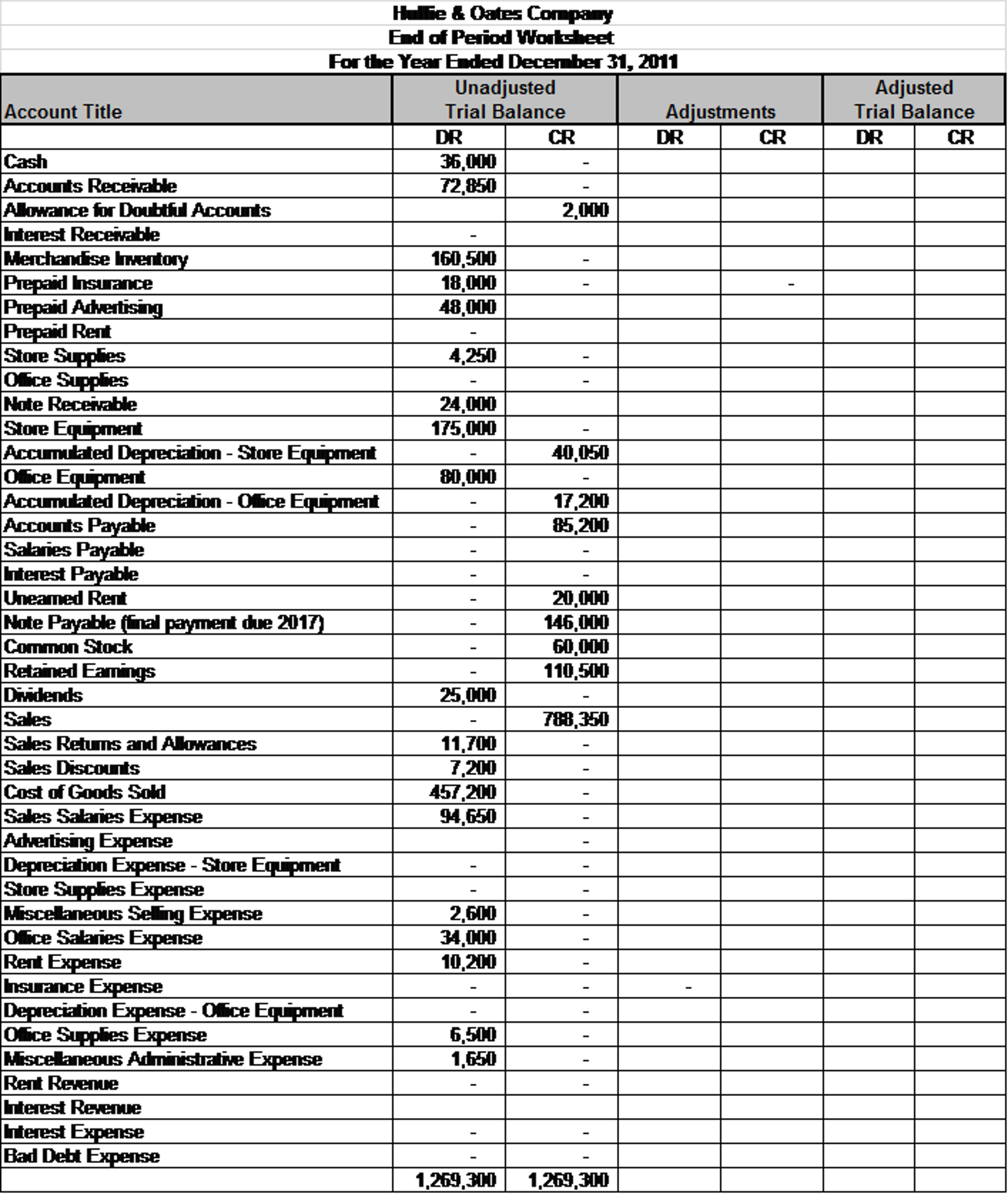

Automation transforms the process of closing entries in accounting, making it more efficient and accurate. By leveraging automated systems, businesses can ensure that all tasks related to closing entries are handled seamlessly, reducing manual effort and minimizing errors. Once we have made the adjusting entries for the entire accounting year, we have obtained the adjusted trial balance, which reflects an accurate and fair view of the bakery’s financial position.

What is the approximate value of your cash savings and other investments?

All revenue and expense accounts must end with a zero balance because they’re reported in defined periods. A hundred dollars in revenue this year doesn’t count as $100 in revenue for next year even if the company retained the funds for use in the next 12 months. Businesses can easily open and close accounts every period by using accounting software to track all financial transactions throughout a given period.

Get in Touch With a Financial Advisor

Now that all the temporary accounts are closed, the income summary account should have a balance equal to the net income shown on Paul’s income statement. Now Paul must close the income summary account to retained earnings in the next step of the closing entries. The first entry requires revenue accounts close to the IncomeSummary account. The process of closing entries in accounting ensures the temporary accounts have a balance of zero at the end of the period. The funds must be transferred into another account, the income summary account, to bring each account balance down to zero.

Do you already work with a financial advisor?

Within this time it will have also incurred expenses of $9,000. In this example, it is assumed that there is just one expense account. In addition, if the accounting system uses subledgers, it must close out each subledger for the month prior to closing the general ledger for the entire company. If the subsidiaries also use their own subledgers, then their subledgers must be closed out before the results of the subsidiaries can be best payroll software for accountants transferred to the books of the parent company. Since the income summary account is only a transitional account, it is also acceptable to close directly to the retained earnings account and bypass the income summary account entirely. The net result of these activities is to move the net profit or net loss for the period into the retained earnings account, which appears in the stockholders’ equity section of the balance sheet.

The Retained Earnings account balanceis currently a credit of $4,665. Printing Plus has a $4,665 credit balance in its Income Summaryaccount before closing, so it will debit Income Summary and creditRetained Earnings. However, if the company also wanted to keep year-to-dateinformation from month to month, a separate set of records could bekept as the company progresses through the remaining months in theyear. For our purposes, assume that we are closing the books at theend of each month unless otherwise noted. Notice that the Income Summary account is now zero and is ready for use in the next period. The Retained Earnings account balance is currently a credit of $4,665.

The statement of retained earnings shows the period-ending retained earnings after the closing entries have been posted. When you compare the retained earnings ledger (T-account) to the statement of retained earnings, the figures must match. It is important to understand retained earnings is not closed out, it is only updated. Retained Earnings is the only account that appears in the closing entries that does not close. You should recall from your previous material that retained earnings are the earnings retained by the company over time—not cash flow but earnings.

The third entry closes the Income Summary account to Retained Earnings. The fourth entry closes the Dividends account to Retained Earnings. The information needed to prepare closing entries comes from the adjusted trial balance. This means that it is not an asset, liability, stockholders’ equity, revenue, or expense account. The account has a zero balance throughout the entire accounting period until the closing entries are prepared. Therefore, it will not appear on any trial balances, including the adjusted trial balance, and will not appear on any of the financial statements.

And so, the amounts in one accounting period should be closed so that they won’t get mixed with those in the next period. As you will see later, Income Summary is eventually closed to capital. Prepare the closing entries for Frasker Corp. using the adjustedtrial balance provided. Notice that the Income Summary account is now zero and is readyfor use in the next period.